[ad_1]

I haven’t had a lot of success investing in real estate, at least not directly. That’s why I don’t talk about real estate investing more than I do.

But about fours years ago I started investing in real estate crowdfunding through Fundrise, and I’m happy to say I’ve been making money at it.

I’d heard about Fundrise before, and it seemed like an opportunity to invest in real estate without losing my shirt. But as has become my way over the years, I decided to jump in and give it a try. For me, that’s the best way to learn.

That was four years ago, and I recently got a congratulatory notice from Fundrise on my “anniversary”. That made now seem like a good time to look back and see exactly how the investment has performed.

It’s not just a matter of looking at that performance either. I also want to know how that performance compares with the results from real estate in general, from competing real estate investments, and also with non-real estate investments.

I hope you don’t mind that we’ll be crunching a bunch of numbers here. But that’s the only way to know what’s really happening when it comes to investing.

Who is Fundrise?

Fundrise got started in 2012, and they’ve since become one of the top platforms in the real estate crowdfunding space They may even be the top platform. Through 2019, they’ve originated $1.1 billion in commercial real estate transactions. That includes both equity and debt investments in properties with a total value of $4.9 billion.

As of February, 2021, the total value of real estate investments is at $5.1 billion, and the company has paid an incredible $100 million in dividends to investors.

Private REITs

Back when I was a financial planner I got involved in private real estate investment trusts (REITs). These are similar to Fundrise, so I am familiar with the concept.

As a financial planner, you love selling these investments. That’s because they paid commissions of between 7% and 10% of the investment made. If a client made an investment of $100,000, you could earn $7,000 or more in commission income. What financial planners like just as much is that when the investor sells their position, they usually weren’t aware of the commission they paid.

Some of the private REITs did quite well – that is, until the real estate crash in 2008. It was worse than just the declines in the value of the trusts. In the middle of the Great Recession, tenants were breaking their leases, cash flow dried up, and investors wanted their money back.

At that point, the problem was that the principals who were running these private REITs didn’t have any cash to pay back the investors. It was a liquidity crisis, which meant it was almost impossible to recover even part of your investment.

That’s not an impossible outcome with private REITs. Buried in the fine print is language advising investors there may be circumstances where they can lose some or all their investment. But as you can imagine, few investors go into any type of investment with the idea that they’re going to lose money on their investment, let alone lose the whole amount.

It even happened to a friend of mine, or really a friend’s mother. She put $100,000 or $200,000 into a private REIT, then got the letter informing her it was all gone.

That’s not quite how Fundrise works, which a big part of the reason I like them.

The Fundrise Solution

What you have with private REITs is a combination of high risk and a lack of transparency on the fees connected with the investment.

That’s exactly what Fundrise set out to remedy. Fundrise investments have lower fees and full transparency in disclosing those fees.

What’s even more important is that you don’t need $100,000 or more to invest. You can invest with as little as $500, which means almost anyone can participate. Even if you do take a loss on an investment that small, it’s probably not the kind that will wipe you out financially the way private REITs did to some investors in the last recession.

Fundrise does disclose the risks of commercial real estate investing. That , includes the possibility you may not be able to liquidate your position.

Just before the COVID pandemic, I got a couple of notices from Fundrise making that point clear. The letters emphasized that if the market were to take a big dive, Fundrise might be forced to halt investment redemptions.

That’s just an inherent risk with commercial real estate investments, simply because real estate – and especially commercial real estate – is not a liquid investment. Unlike a mutual fund, a private REIT can’t sell stock to raise cash to pay investors. It’s also close to impossible to sell an office building or an apartment complex in a bad market where there’s probably no buyers.

It’s unavoidable, but I give Fundrise credit for updating their investors about this possibility on a regular basis.

With Fundrise, there are no upfront fees, and you’ll know exactly what you’ll be getting into – including the fees you pay along the way.

Other Real Estate Crowdfunding Platforms

Fundrise isn’t the only real estate crowdfunding platform out there. There are others that provide similar opportunities, also offering low investments and transparent fee structures.

YieldStreet works similar to Fundrise in that they offer investments in commercial real estate. But they also include alternative investments, like marine loans, artwork, and private business credit. It’s probably better suited to more sophisticated investors with a big appetite for risk.

Groundfloor also invests in commercial real estate, but not in the same way as Fundrise. Instead of offering equity investments, and an opportunity for long-term growth, they focus on investing in financing for commercial projects. You can invest with as little as $10, and the investments are short-term – generally less than one year.

DiversyFund is another real estate crowdfunding platform that invests in commercial real estate. But they focus primarily on large apartment complexes, which they feel are better long-term investments. You can invest in their REIT with as little as $500.

I think RealtyMogul is probably the closest competitor to Fundrise. You can begin investing with as little as $1,000, but the deals they invest in are much more specialized. For example, you can invest in individual properties. But the one catch with RealtyMogul is that you must be an accredited investor, which means you must meet certain pretty strict financial criteria to qualify.

The fact that there are multiple real estate crowdfunding platforms in the market confirms a strong demand for this type of investment. But just as important, the competition forces each platform to provide a better investment offer to their customers.

How Do You Get Started with Fundrise?

One of the big advantages with Fundrise is that they have their product on their website, and they even offer mobile access. This is unlike those private REITs I was talking about earlier, where information is hard to find, and often buried in the fine print. Fundrise puts it all out there, so you’ll know exactly what’s going on at all times.

You can sign up for an account directly on the Fundrise website. It’s free to open an account, and you can choose both the amount you want to invest, and the specific plan that will work best for you.

Fundrise offers four different plans, which I’ll go into in detail in the next section.

Fundrise Plans & Portfolios

Fundrise offer four portfolios, Basic, Core, Advanced and Premium. But if you’re new to investing in commercial real estate, you may want to consider the Starter Plan.

Starter Plan

One of the features of Fundrise I really like is their Starter Portfolio. I know there are other investors like me, who will have at least a little bit of fear about investing in commercial real estate. But that’s what this plan is all about.

You can invest in the Starter Plan with just $500, which is free to open. That’s a small investment, but it actually provides an impressive amount of diversification. Not only do they invest in commercial properties, like office buildings and apartment complexes, but they also include single-family real estate investments. You also get geographic diversification, since the properties held in the portfolio are located across the country.

Basic

With an investment of $1,000, you can invest in their Basic Plan. That plan gives you access to dividend reinvesting, auto invest, and the ability to create and manage your investment goals. The Basic Plan also gives you three months fee-free for each friend you invite to Fundrise who opens and funds an account.

Core

Next is the Core Investment Strategy, which requires a minimum investment of $5,000. That comes with all the features of the Basic Plan, plus Fundrise’s private eREIT fund, as well as the ability to customize your investment strategy.

This is the plan I have right now, and it includes three different investment strategies:

- Supplemental Income – this is the plan you would choose if your primary interest is generating a regular income.

- Long-term Growth – this is like investing in the stock market, where you’ll be looking primarily at long-term capital gains.

- Balanced Investing – this option offers you a mix of supplemental income and long-term growth.

Advanced

The Advanced Plan requires a minimum investment of $10,000. With this plan, you’ll have all the features and benefits of the other three plans, but you’ll get nine months of fees waived for each friend you invite to join Fundrise. (They don’t say if the fee waiver applies only on friends who sign up for the $10,000 plan, or if it extends to any plan Fundrise offers.)

Premium

Finally, there’s the Premium Plan, and requires a minimum investment of $100,000. I’m not going to dig into this one, because it’s probably beyond the scope of what most readers of this blog are looking for, or even what I would consider.

My Fundrise Portfolio

I started my Fundrise investment in February 2018 with $1,000 in the Basic diversified portfolio plan. About a month later, Fundrise was offering an initial public offering (IPO), which is something that always grabs my attention.

But to take advantage of the IPO, I had to have at least $5,000 invested, and that meant moving up to the Core plan. That was as easy as adding an additional $4,000 to my original investment.

The current balance of my account is about $11,113.83. Of that, $8,055.99 is the growth of the original $5,000 investment. The remaining balance in the account is my portion of the Fundrise IPO.

Focusing only on the real estate side, my $5,000 investment has increased by $3,055.99 over just four years.

Here’s how that breaks down by annual percentage return:

- 2018: 7.4%

- 2019: 9.2%

- 2020: 7.6%

- 2021: 23.9%

- 2022 YTD: 2.7

- Average annual return: 13.3%

I don’t have the full dollar breakdown for each year, but here’s what I do have, along with the split between dividends and capital appreciation:

- 2018: Dividends, $274; capital appreciation, $74, for a total return of $348, net of fees.

- 2019: Dividends, $383; capital appreciation, $131; advisory fee, $7.97, for a net total return of $506.

- 2020: Dividends, $226; capital appreciation, $234, for a total return of $452, net of fees.

- 2021: Dividends, $229; capital appreciation, $1,308.36, for a total return of $1,528 net of fees

- YTD, through March, 2022: Total return of $219, net of fees.

- Total net return for all four years: $3,055.86

This is what I really like! They break down exactly how much you earn, and also where you earn it. They also let you know when a property has been sold. All that information is available in the Fundrise dashboard.

As a comparison of my returns here’s what Fundrise shares on their site:

My Specific Portfolio Allocations

I was most interested in long-term growth, so I invested in the Growth REIT. They also offer the East Coast, West Coast, and the Heartland (Midwest) REITs.

But in looking at the distribution on my pie chart, it says I have 36% invested in fixed income, 15% in Core Plus, 33% in Value Add (typically, renovation projects), and 15% in Opportunistic.

Not only do I always know what I’m investing in, but Fundrise even gives me pictures of what I’m invested in. For example, one holding is a $5.8 million construction project, Mosby University City. It’s a 300-unit apartment complex in Charlotte, North Carolina, and they’ve announced that it’s recently been completed.

Another example is the recent investment into a single-family rental development near Dallas, Texas. It gives you the strategy, which is Opportunistic, and the total value of $16.5 million. Others are projects in Atlanta, Los Angeles, and Austin, Texas. They even discloses some investments, located near where I live.

The point is, I know where my money is being invested at all times.

How Do Fundrise Returns Compare with Other Investments?

So I have an average annual return with my Fundrise investment of 13.3% in just over four years. But is that a good return?

It all centers on the basic question: “What if I had invested my money in something else?”

That can include other real estate investments, as well as stocks and crypto.

It really depends on what your investment goals are, and what you compare those returns with.

Fundrise vs. Other Real Estate Investments

To recap, my four-year average return on my Fundrise investment was 13.3%, net of expenses.

I can’t do a valid comparison among other real estate crowdfunding platforms since I’m only invested with Fundrise.

But we can look at the Fundrise returns against those provided by real estate exchange traded funds (ETFs), which are widely available on market exchanges.

Fundrise vs. the VNQ

Probably the most popular is the Vanguard Real Estate ETF (VNQ). This isn’t a full apples-to-apples comparison, because I didn’t start my Fundrise investment until roughly the end of the first quarter of 2018.

Even still, in 2018 my net return with Fundrise was 7.4%. This compares with a -5.9% for the VNQ. That’s a more than 13% difference between the two investments, and I’d rather make money then lose it.

For 2019, my Fundrise return was 9.2%. VNQ had a return of 28.89%. Even though I made over 9%, it definitely hurt that VNQ made almost 29%. For 2019 at least, it was a 20-point swing against Fundrise.

What about 2020? Fundrise returned 7.6% for the year, while VNQ was down 4.64%. That’s a swing of more than 12% in my favor.

The performances in 2018 and 2020 were no-brainers in favor of Fundrise. But if I had started investing in 2019, the investment with Vanguard would have produced a return three times greater than what I got with Fundrise for that year.

That’s a tough difference to swallow, and if it were happening on a consistent basis I certainly wouldn’t be happy with Fundrise. Anytime an investment consistently underperforms the competition, it’s just about the best evidence you’re in the wrong investment.

But Fundrise demonstrated a major advantage over VNQ…

The Fundrise Consistency Factor

Even though VNQ made Fundrise look bad in 2019, it easily outperformed Vanguard in two out of three years.

When I did a three-year calculation of the average annual returns from Vanguard, it came to 6.093%. That was well below the 8.1% average with Fundrise.

But with that said, a quick look at the year-to-date return on VNQ for 2021 shows a positive return of 13.54% through the end of April. When compared with the 1.9% year-to-date return from Fundrise, it’s possible VNQ pulled ahead, or that the returns between the two are very close.

Even still, the fact that Fundrise has had three consecutive positive return years is also important. One of the primary challenges for any investor is to avoid losing money. That would be the case with a Fundrise investment over the past three years, while VNQ turned losses in two out of those years.

Consistency matters with investing.

Fundrise vs. the REET

Let’s take a look at another example of the real estate front, iShares Global REIT ETF (REET).

This again is not exactly an apples-to-apples comparison. Where VNQ is a US-based ETF, REET takes in real estate investments from around the world.

Similar to the VNQ, REET was down in 2018 by 4.89%. In 2019 it was up by 23.89%, then down 10.59% in 2020. I’m not going to break down the numbers with this one, because it’s pretty easy to see that REET underperformed both Vanguard and Fundrise on an average annual basis.

In looking at these two potential real estate investments, I’m not having any buyer’s remorse over my decision to invest with Fundrise. It outperformed both alternatives over three years.

Fundrise vs. The Stock Market

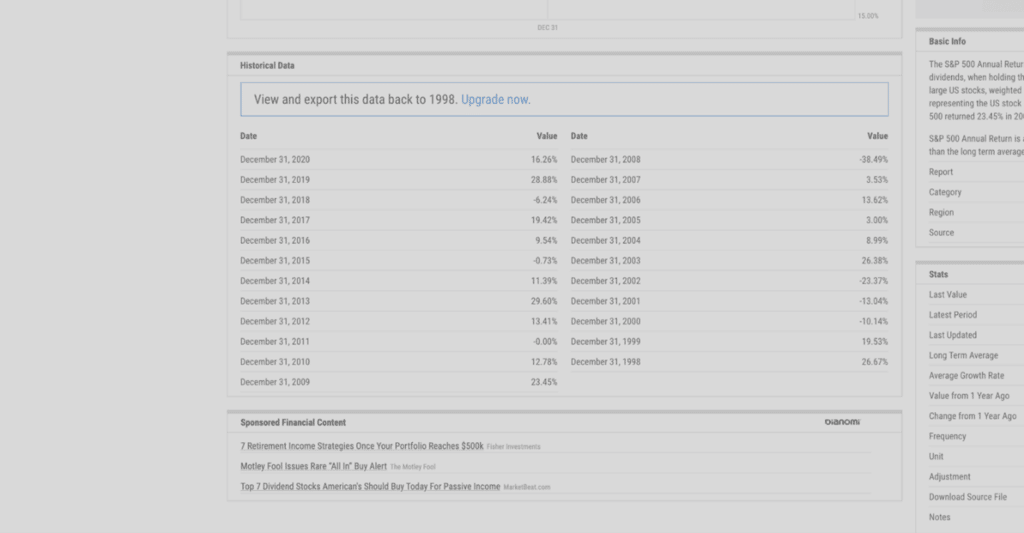

For 2018, the S&P 500 index was down 6.24%. In 2019, it was up 28.88%. And in 2020, is up 16.26%. Through April 2021, we’re looking at an incredible 57.9% gain.

Well, but those are crazy returns – especially in the middle of a global pandemic. And I don’t know that we’ll ever see returns like that again.

When I average out the returns on the S&P 500 index over the past three years and comes to 12.96% per year. That’s almost 5% per year more than my Fundrise investment paid.

(Source: YCharts)

So clearly, if I had invested my $5,000 Fundrise investment in the S&P 500, I’d have come out ahead. That’s a definite investment opportunity cost.

Fundrise vs. Crypto

Let’s go beyond stocks and other real estate investments and look at Fundrise compared with a true alternative investment: cryptocurrency.

This isn’t an arbitrary comparison either. I’ve been invested in crypto since 2018, along with my Fundrise investment.

We’re doing this just for fun, because certainly comparing real estate crowdfunding with crypto is about as far away from an apples-to-apples comparison as you can possibly get. But let’s do it anyway!

We’ll compare Fundrise with Bitcoin. The total return for that crypto in 2018, was -72.6%. But that comes after 2017, when Bitcoin had a return of 1,318%.

But the situation changes in the next two years. Bitcoin is up 87.2% in 2019, and 302.8% in 2020. What’s more, Bitcoin continued to power forward in the first few months of 2021.

Looking at the average annual return on Bitcoin for 2018, 2019 and 2020, it’s an unbelievable 105%.

Fortunately, I was invested in the stock market and crypto at the same time I was in Fundrise, so I didn’t miss out. But now you have a side-by-side comparison of how Fundrise performs compared to both commercial real estate and non-real estate investments, like stocks and crypto.

My Thoughts on Fundrise

We’ve crunched a lot of numbers in this analysis, but I need to point out that investing isn’t all about returns alone. More important is, what is your goal with your money? Or more specifically, what are you hoping to use the money for?

For example, if you’re looking to save money to make a down payment on a house, or to retire early, an investment in Bitcoin that drops more than 72% in the first year isn’t going to get the job done.

Something else I want to point out is that the returns in the market over the past few years have been phenomenal, but they’re not typical. A correction is going to happen at some point, and when it does investments in stocks and even crypto will take a big hit.

I’m not trying to spread doom and gloom and advise putting all your money into safe investments. But we all need to be ready for a correction. They are going to be losses, which we saw in both the Vanguard and iShares ETFs in 2018 and 2020.

Making Fundrise Part of a Balanced Portfolio

For me, I want a diversification into real estate, but I’m not qualified to invest in individual properties. I’m not interested in buying, renting, managing and selling property, but I want the diversification real estate provides.

I did put money into a private REIT in my self-directed IRA, but that’s primarily for long-term investing for my retirement. It’s a completely passive investment, which is exactly what Fundrise does for me outside my IRA.

I use the “barbell investment method”. That means I have a lot of money invested in safe investments, and a small amount invested in high risk/high return investments. But I don’t have much in the middle, which is basically what Fundrise is. So for me, returns aside, Fundrise has a definite place in my portfolio. It gives me exposure to the commercial real estate market, plus regular updates on what’s going on in my portfolio.

A big part of building wealth is being involved in various investments so that I can know what’s going on with different asset classes. That doesn’t happen unless I’m actually invested in those asset classes.

If you want commercial real estate in your portfolio, I recommend Fundrise. It’s requires only a small investment, provides plenty of investment options, low and transparent fees, and you’ll always know what’s going on with your money.

[ad_2]

Source link