")

[ad_1]

Chances are, you’ve heard someone mention the term compound interest, at some point. But do you know exactly what it is and how it can benefit your investments? And just as important, do you know where to find the best compound interest investments?

Whether you are an active investor or an aspiring one, it’s crucial that you understand how compounding works. In my estimation, compound interest is critical to successful investing.

In this article, I’ll explain compound interest, how it works, and how you can use compounding to your advantage in your portfolio.

What Is Compound Interest?

Compound interest is earning interest on the interest you’ve already made.

Imagine a rolling snowball. A small snowball – representing your initial investment – gradually becomes larger as it rolls forward and adds more snow to what’s already stuck to the snowball. The more snow (interest) the snowball (your initial investment) takes on, the bigger the snowball becomes (your final investment).

That’s what compound interest can do with your savings and investments.

You could argue that compound interest is the secret sauce of successful investing.

An Example of Compound Interest

For those of you who like to see the numbers, here’s an example of compound interest at work:

Suppose you invest $1,000 in a five-year certificate of deposit, paying 5% and compounded annually.

The compounding will look like this:

- At the end of the first year, your CD balance will grow to $1,050. That includes your original investment of $1,000 plus $50 in interest earned.

- At the end of the second year, your CD balance will be worth $1,102.50. The amount includes $1,000 original investment, $50 in interest earned in the first year, $50 in interest earned in the second year, plus $2.50 earned on the $50 in interest you earned in the first year of the CD.

- At the end of five years, your CD will have grown to $1,276.28. From that, $26.28 is compound interest earned on your interest over the same five years.

The $26.28 in compound interest isn’t significant, but we were basing it on a modest $1000 investment and a relatively short, 5-year time frame.

The figure would be much higher if you started with a larger amount, made regular contributions, and invested for 20 or 30 years.

You could argue that compound interest is the secret sauce of successful investing.

One of them, at least.

What Is the “Rule of 72”?

The Rule of 72 is a simple formula used to determine the years it will take for a certain investment to double in value based on a given interest rate.

The table below illustrates how many years it will take for $1,000 to double at various interest rates (daily compounding) The Calculations are performed using the Calculator Soup Rule of 72 Calculator.)

| Interest Rate | Actual Number of Years to Double Your Investment | Rule of 72 Calculation |

| 1% | 69.66 | 1% divided by 72 = 72 years |

| 2% | 35 | 2% divided by 72 = 36 years |

| 3% | 23.45 | 3% divided by 72 = 24 years |

| 4% | 17.67 | 4% divided by 72 = 18 years |

| 5% | 14.21 | 5% divided by 72 = 14.4 years |

| 6% | 11.9 | 6% divided by 72 = 12 years |

| 7% | 10.24 | 7% divided by 72 = 10.29 years |

| 8% | 9.01 | 8% divided by 72 = 9 years |

| 9% | 8.04 | 9% divided by 72 = 8 years |

| 10% | 7.27 | 10% divided by 72 = 7.2 years |

As you can see from the calculations in the table, the Rule of 72 is just an approximation, a rule of thumb. Also, the higher the interest rate, the more exact the Rule of 72 calculation becomes.

Mixing Compound Interest with Regular Contributions

We’ve already seen how compound interest causes accelerates investment growth. But the effect is even greater when you add regular contributions to the mix. That’s how retirement plans and other investment vehicles work.

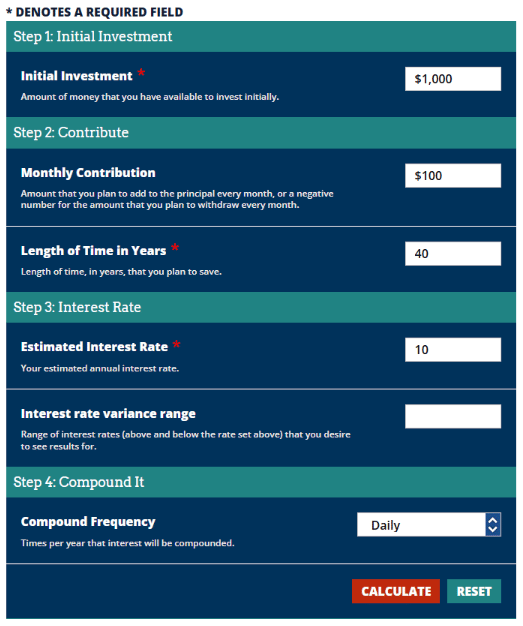

Here’s an example, using an initial investment of $1,000, adding $100 in monthly contributions and 10% interest (compounded daily) for 40 years. We’ll use the Compound Interest Calculator from Investor.gov to show how this works.

The input will look like this:

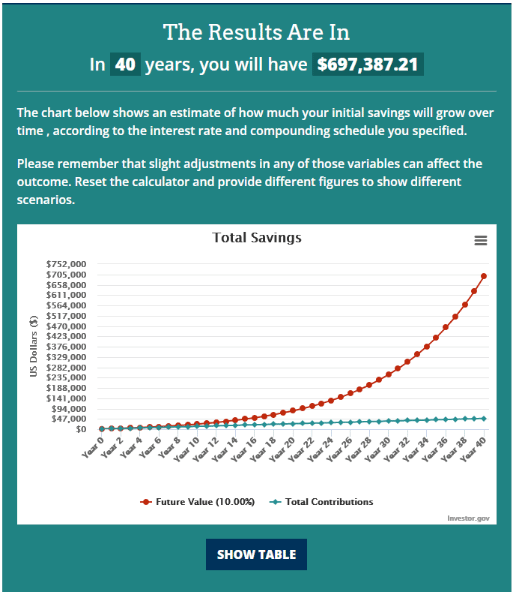

The results are as follows:

From an initial investment of $1,000, the combination of compound interest and regular monthly contributions caused this investment to grow to nearly $700,000!

This is why compound interest – combined with regular monthly contributions – is the small investor’s greatest strategy to build wealth. (Or any investor, for that matter.)

Neither dollar figure is beyond the reach of a person of even modest financial means. The initial investment of $1,000 is less than many people have sitting in an emergency fund. And many people can afford to make a $100 monthly contribution via direct payroll contributions.

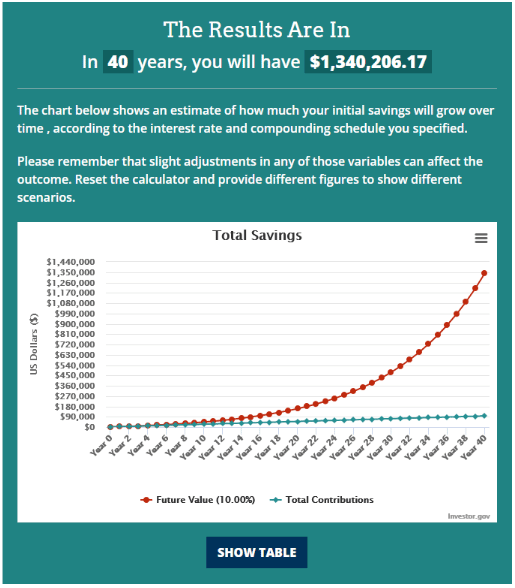

But let’s take it a step further – using the same information but increasing the monthly contribution to $200, how will things look at the end of 40 years?

The investment doubles from just under $700,000 to about $1.34 million!

That’s the power of compound interest, which is why would-be investors need to embrace the concept as early in life as possible.

What Types of Accounts are Best for Compounding?

Now that you see what compound interest can do to your investments let’s look at where and how you can make that compounding happen.

Banks Savings Accounts. Most savings accounts, money market accounts, and certificates of deposit earn compound interest. However, they fall into the safest asset class, so you won’t get the highest returns.

Discount Brokerages. You can buy just about any investment through an online broker, including bank products like CDs. But it’s also where you’ll find other interest-bearing assets, like corporate bonds, U.S. Treasury securities, municipal bonds, and bond funds. The variety of investment vehicles means you’ll have a better chance of earning higher returns than you can at a bank.

Cryptocurrency exchanges. This is a surprise to anyone who doesn’t invest in crypto. But crypto exchanges aren’t just the place to buy and sell crypto. Many crypto exchanges also offer high interest on crypto balances. Those returns are usually much higher than you can get in a bank or a bond. If you’re willing to accept some risk (okay, a lot of risk), in exchange for a higher return, crypto exchanges can be a place to park some of your investing cash.

Taxable vs. tax-deferred vs. tax-free accounts. Contributions you make to tax-sheltered plans are often tax-deductible, and the investment income earned within the account is tax-deferred.

If you can avoid paying income tax on your investments for many years, you will build wealth much more quickly than if you invest in a taxable account.

It’s also possible to take advantage of tax-free accounts. Roth IRAs and Roth 401(k)s don’t offer tax-deductible contributions. But the investment earnings within each account accumulate on a tax-deferred basis. And once you reach age 59 ½ and have been in a plan for at least five years, you can begin taking tax-free withdrawals.

Next, let’s look closely at various investments that earn compound interest.

Best Compound Interest Investments

1) Certificates of Deposit (CDs)

A CD is an investment contract you enter into with a bank. In exchange for investing a certain amount of money, the bank will provide you with a guaranteed return of principal, as well as interest earned on the certificate. CD terms range from 30 days to five years, allowing you to lock in an attractive interest rate.

Most banks offer CDs. But if you’re looking for the highest rates possible, you can check out an online CD marketplace like SaveBetter. They have CDs from banks across the country, some paying interest as high as 5.00% APY.

2) High-yield Savings

All banks offer savings accounts, but some pay you more interest than others. A high-yield savings account pays more interest than ordinary savings accounts. Unlike CDs, there’s no guarantee on how long the bank will maintain the same interest rate. It could change at any time.

Even though rates are rising, many banks continue to pay subpar interest. You’ll need to shop to find the institutions with the highest-yielding savings.

An example is ufb Direct. They’re currently paying 3.16% APY on all account balances and with no maintenance fees.

3) Money Market Accounts

There’s not a whole lot of difference between savings accounts and money market accounts anymore. The main difference is that money markets usually allow you to access your account balance with checks, while savings accounts don’t.

Interest rates paid between savings accounts and money market accounts are generally similar. And once again, most banks pay very little interest on these accounts.

ufb Direct also offers high-yield money market accounts, currently paying 3.16% APY. The account offers access by checking, and there is a $10 monthly fee unless you have a minimum balance of $5,000.

4) Bonds

This is a very broad category of interest-bearing securities.

Individual bonds. Bonds are debt securities issued by corporations to expand their operations or to retire old bonds. They’re often issued in denominations of $1,000 and for terms of 20 years. The yield on high-grade corporate bonds is currently around 6%, and 9% on high-yield bonds. High-yield bonds were once known as “junk bonds” because of the higher default risk.

The US Government also makes bonds available, notes (terms of 10 years or less), and bills (terms of less than one year). You can purchase them in amounts as low as $25. Current yields are around 4% or higher.

Corporate bonds can be purchased through investment brokers, while U.S. Treasury securities can be purchased either through investment brokers or at TreasuryDirect.

Series I savings bonds. These are variations of securities issued by the U.S. Treasury. Series I savings bonds, or simply I Bonds, can be purchased in denominations of $25. You can purchase up to $10,000 in I Bonds annually, with a current variable yield of 6.89% APY.

Municipal bonds. State and municipality governments can issue municipal bonds. They work like other bonds, but the interest earned on those bonds is tax-exempt for federal tax purposes. If your state issues bonds, they will be exempt from state income tax. Municipal bonds are usually purchased through an investment broker.

Bond funds and ETFs. You can buy bonds through a bond fund, like a bond mutual fund or ETF. There are all kinds of bond funds you can choose from. For example, funds can focus on short-term, intermediate, or long-term bonds. They can also hold corporate bonds, government bonds, or a mix of both. Some funds invest in foreign bonds. Bond funds can be purchased through investment brokers.

Investments That Compound Quickly

The investments we’ve discussed up to this point combine interest income with a high degree of safety of principal. But if you want higher returns, you can invest in securities with greater risk.

The investments below have varying levels of return as well as risk. You can generally assume higher returns will be available on investments with greater risk.

5) Individual Stocks

Individual stocks don’t pay interest, but many established companies pay dividends to return profits to their shareholders. Dividend rates can rise and fall and are not guaranteed. However, most companies are incentivized to continue paying dividends, and increase them if possible.

The average return on stocks was approximately 12% between 1957 and 2021 when both growth and dividends are factored into the return. Some stocks are considered near recession-proof. Examples include utility, health care, and high-dividend stocks.

But you must be aware of the risk factor with stocks.

While they may provide double returns over the long term, you can experience a decline in value in any given year. That’s the risk/reward factor at play.

You can invest in individual stocks through investment brokers. If you like to choose your own stocks but don’t want to manage your portfolio, check out M1 Finance. It’s a robo advisor that allows you to choose up to 100 stocks or ETFs for your portfolio, all commission-free, then manage the portfolio at no charge. You can even create as many portfolios as you like.

6) ETFs

If you want to invest in stocks but don’t want to choose or manage them, look into an exchange-traded fund (ETF). It works something like a mutual fund in that it holds a portfolio of many individual stocks. ETFs are usually index-based, which means they invest in a recognized stock market index, like the S&P 500.

But the ETF market has become highly specialized. It’s possible to invest in specific stock sectors using a fund. For example, you can invest in energy stocks, healthcare stocks, precious metals, technology, or just about any sector you can imagine.

If you like the ETF concept but don’t want to manage your own portfolio, you can invest through a robo advisor like Betterment. They’ll create an entire portfolio of ETFs invested in both stocks and bonds based on your own investment preferences and temperament. And all for a ridiculously low annual fee.

7) Mutual Funds

Mutual funds are pooled investment funds that are, in most cases, actively managed. Unlike ETFs, which are designed to match the performance of an underlying stock index, a mutual fund manager attempts to outperform market returns. As a result, mutual funds have higher operating costs, which are passed along to the investor through fees, known as Management Expense Ratios (MERs). MERs for actively-managed mutual funds can be as high as 2%.

Mutual funds come in two broad categories, growth funds and balanced funds. As the name implies, growth funds focus on capital appreciation. That means the stocks they hold have a strong orientation toward growth.

Balanced funds include both growth stocks and dividend stocks (and even bonds). The returns on these funds may be lower than on growth funds, but they tend to be more consistent due to the dividend and interest income.

An example of a growth fund is the Vanguard U.S. Growth Fund Investor Shares (VWUSX). The fund actively invests in large US corporations and requires a minimum investment of $3,000. As you might expect, the performance of this fund has been dismal in 2022, down nearly 40%.

The Fidelity Balanced Fund (FBALX) is an example of a balanced mutual fund. Its current composition includes 66% held in stocks and 34% in bonds.

8) Rental Real Estate

While real estate doesn’t earn interest like a savings account or CD, it allows you to compound your income by combining rental income and capital appreciation.

There are different ways to invest in real estate. The first and most common is buying a principal residence. Or you can buy a vacation home, which can be held primarily for long-term capital appreciation. However, that can be a money loser if it doesn’t generate any rental income.

A more effective way to invest in real estate is by purchasing rental real estate. This can include everything from a single-family house to investing in apartment buildings.

One portfolio-friendly way to invest in physical real estate is through Roofstock. It’s an online real estate marketplace where you can select single-family properties to invest in. Roofstock fully vets the properties, and they require a 20% down payment on each property you purchase.

9) Real Estate Investment Trusts (REITs)

A real estate investment trust, or REIT, is like a mutual fund that holds commercial real estate. A REIT can specialize in specific property types, like retail space, office buildings, large apartment complexes, or warehouse space. You can purchase shares in a REIT the same way you would buy company stock. You can buy and sell REITs through investment brokerage firms.

If you want to invest more directly in specific real estate activities, consider purchasing shares in large homebuilder companies or the many companies that supply building materials to the construction industry.

There are also mutual funds and ETFs that specialize in real estate. For example, the Vanguard Real Estate ETF (VNQ) invests in various REITs. Fidelity® Select Construction and Housing Portfolio (FSHOX) invests in both homebuilders and construction supply companies.

Yet another option is crowdfunded real estate platforms. These are online real estate investment platforms that enable you to invest in non-publicly traded REITs.

Two popular examples are Fundrise and Realty Mogul. Fundrise is suitable for new and small investors due to its $10 minimum investment. RealtyMogul has a much higher minimum investment ($5000) but invests in real estate equity and debt deals, normally reserved for institutional investors.

10) Alternative Investments

Alternative investments fall outside conventional investing categories, like stocks and bonds or savings accounts and CDs. The risks can be high, but so are the potential rewards. In the past alternative investments have been off-limits to the average investor, but these days you can invest more easily invest in alternative investments via several online platforms.

For example, you can use YieldStreet to invest in unusual asset classes like legal notes, real estate, fine art, and airplanes. The minimum investment required is $1,000. Because these are alternative assets, you must be an accredited investor to participate.

Mainvest is another platform where you can invest in alternative assets, but a very specific one. With as little as $100, you can lend money to small businesses. Those loans carry expected returns of between 10% and 25%. You don’t need to be an accredited investor to participate in this platform.

11) Crypto

You’re probably already aware of cryptocurrencies’ potential gains (and losses). Two of the most popular coins are Bitcoin and Ethereum. The obvious play with both these cryptos is the potential for large gains in value. Bitcoin, for example, started at about $1 in 2009 and rose to nearly $69,000 by 2021. It’s since settled back to $20,000, but that may be setting it up for the next big move upward.

As mentioned, you can earn high interest on your crypto balance through certain crypto exchanges.

Gemini, a popular crypto exchange, is currently advertising paying up to 8.05% APY on crypto balances. That’s about double the rate you can get on U.S. Treasury securities. Remember that while these rates are admittedly high, the FDIC will not insure your deposits.

12) Art

This asset category isn’t so much about compound interest as it is about long-term speculative growth. Fine art has proven to be a great long-term investment, but until recently, only the wealthy have had access.

An online platform called Masterworks aims to change all that. They sell shares in popular fine works of art at $20 a share. With a minimum investment of $1,000, you can invest in 50 pieces of artwork.

Again, it’s speculative in nature but has the potential to pay handsomely over the very long term.

13) Wine

This asset class is similar to fine art, except it involves fine wines. A company called Vinovest claims to be the world’s leading wine investment platform, and they’ll enable you to invest in fine wines with a minimum investment of $1,000. According to Vinovest, fine wines have provided an average annual return of greater than 10% over the past 30 years.

14) Collectibles

Collectibles can be purely speculative, but the return potential is high. A Mickey Mantle baseball card , for example, sold for $12.6 million earlier this year. This is a one-in-a-million opportunity that you would never find if you went looking for it. But it does indicate what’s possible.

There’s no way to know if a given collectible will appreciate in value, certainly not to that degree. But when you see the potential, it can make beginning the search worth considering. Other collectibles include cars, vintage toys, sneakers, and coins.

Final Thoughts on the Best Compound Investments

Investments that earn compound interest offer a ton of potential over the long term. The good news is that plenty of investments allow you to compound your income, from safe, low-yielding bank accounts and CDs to stocks, investment funds, and more.

If you have never invested, now is the time to start! Remember, the longer your money is invested, the more it can compound. If you already have investments, take a look at your portfolio. Are you missing out on compound growth opportunities? If so, look for ways to incorporate compounding in your portfolio.

FAQs on Compounding Investments

The amount of compounding interest accrued on a loan or deposit over time is determined by the frequency of compounding and the size of the initial principal. For example, if you borrow $100 at 10% interest, with monthly compounding, you will owe $110.63 at the end of the first month, $121.29 at the end of the second month, and so on.

To calculate the compounding interest for a given number of periods, use the following formula:

A = P(1 + r/n)^nt

Where:

A = The amount of compounding interest accrued

P = The initial principal

r = The annual interest rate (divided by 100 to convert to a decimal)

n = The number of periods per year

t = The number of years

Compound interest is when the interest that gets accrued on a sum of money gets reinvested back into the account in addition to the initial deposit. This causes the total amount of money in the account to grow at an accelerated rate. The longer the money stays in the account, the more compounded interest will be earned, which will result in a larger final balance.

The compound interest investment that earns the most money is the one with the highest annual percentage yield (APY). The best compound interest investments are typically those that offer the highest returns with the least amount of risk. Some of the most common options include stocks, bonds, and mutual funds.

Other options include:

-High Yield Savings Accounts

-Certificates of Deposit (CDs)

-Treasury Inflation Protected Securities (TIPS)

-Municipal Bonds

-Corporate Bonds

-Dividend Stocks

Yes, compounding interest can make you rich, but it all depends on how much you save and how long you let your money grow. Over time, the effects of compounding can be quite powerful, so it’s important to start saving as early as possible. If you’re able to consistently save money and let it grow over a long period of time, you could eventually become a millionaire!

[ad_2]

Source link