![Roth IRA Rules + Contribution Limits [2023 Update]](https://i2.wp.com/www.goodfinancialcents.com/wp-content/uploads/2022/12/2023-roth-ira-income-limts-1024x656.png?ssl=1 "Roth IRA Rules + Contribution Limits [2023 Update]")

[ad_1]

Opening a Roth IRA can be a smart move if you want to invest for retirement and save money on taxes later in life. However, there are strict rules when it comes to how much you can contribute to your Roth IRA.

Contributions to a Roth IRA are made with after-tax dollars, which means your money can grow tax-free. When you’re ready to take distributions from your Roth IRA in retirement (or after age 59 ½), you won’t pay income taxes on your distributions, either.

If you want to start contributing to a Roth IRA as part of your retirement strategy, keep in mind there are some limits. For example, if you’re under the age of 49 you can contribute a maximum of $6,500 for the 2023 tax season.

Interested in learning more about the specifics of the Roth IRA? Here’s everything you need to know.

How Much Can You Contribute to a Roth IRA?

For the 2023 tax season, standard Roth IRA contribution limits remain the same from last year, with a $6,500 limit for individuals. Plan participants ages 50 and older have a contribution limit of $7,500, which is commonly referred to as the “catch-up contribution.”

You can also contribute to your IRA up until tax day of the following year.

| Contribution Year | 49 and Under | 50 and Over (Catch Up) |

| 2023 | $6,500 | $7,500 |

| 2022 | $6,000 | $7,000 |

| 2020 | $6,000 | $7,000 |

| 2019 | $6,000 | $7,000 |

| 2018 | $5,500 | $6,500 |

| 2017 | $5,500 | $6,500 |

| 2016 | $5,500 | $6,500 |

| 2015 | $5,500 | $6,500 |

| 2014 | $5,500 | $6,500 |

| 2013 | $5,500 | $6,500 |

| 2012 | $5,000 | $6,000 |

| 2011 | $5,000 | $6,000 |

| 2010 | $5,000 | $6,000 |

| 2009 | $5,000 | $6,000 |

What You Need to Know About Roth IRAs

Here’s the thing about opening a Roth IRA: not everyone can use this type of account. We’ve included a few important Roth IRA rules you need to know about below.

Fund Distributions

Roth IRA accounts come with a few unique benefits outside of future tax savings. For example, you don’t have to take Required Minimum Distributions (RMDs) out of a Roth IRA at any age, and you can leave your money in your account for as long as you live.

You can also continue making contributions to a Roth IRA after you reach age 70 ½ provided you earn a taxable income that’s below Roth IRA income limits.

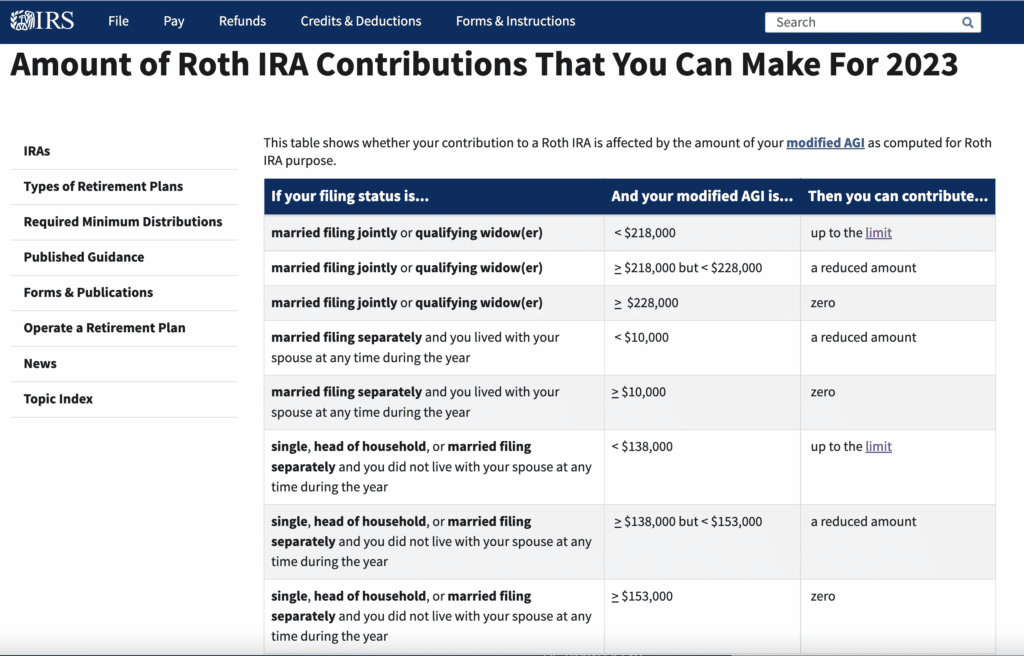

Roth IRA Income Limits

Not everyone can contribute into a Roth IRA account due to income caps. There are income guidelines that must be followed — it’s even possible to have an income so high you can’t use a Roth IRA at all.

If your taxable earnings fall within certain income brackets, your Roth IRA contributions might be “phased out”. This means you can’t contribute the full amount toward your Roth account.

Here’s how Roth IRA income limits and phase-outs work, depending on your tax filing status.

Married couples filing jointly:

- Couples with a modified adjusted gross income (MAGI) below $218,000 can contribute up to the full amount.

- Couples with a MAGI between $218,000 and $227,999 can contribute a reduced amount.

- Couples with a MAGI of $228,000 or more can’t contribute to a Roth IRA.

Married couples filing separately:

- Couples with a MAGI below $10,000 can contribute a reduced amount.

- Couples with a MAGI of $10,000 or more can’t contribute to a Roth IRA.

Single tax filers:

- Single tax filers with a MAGI below $138,000 can contribute up to the full amount.

- Single tax filers with a MAGI between $138,000 and $152,999 can contribute a reduced amount.

- Single tax filers with a MAGI of $153,000 or more can’t contribute to a Roth IRA.

Retirement Account Conversions Allowed

If you have another type of retirement account, like a traditional IRA or even a workplace 401(k), it might be tempting to convert this account into a Roth IRA. This is known as a Roth IRA conversion which requires you to pay income taxes on your distributions now so you can avoid income taxes later on.

Although that might sound aggressive and unnecessary, there are many scenarios where a Roth IRA conversion can make sense. For example, let’s say you’re not earning a lot of money in a specific year and you want to convert to a Roth IRA while paying an extremely low tax rate. You could fork over the taxes now and avoid paying income taxes on distributions later in life when you’re taxed at a higher rate.

As mentioned earlier, Roth IRA accounts don’t require you to take a minimum distribution while you’re alive. Moving your money into a Roth IRA can make sense if you don’t want to be forced into required minimum distributions (RMDs) like you would with a traditional IRA or a 401(k) at age 72.

With a Roth IRA conversion, you’d create an opportunity where your money could grow and compound, untouched, for a much longer stretch of time.

IRA Recharacterization

A recharacterization takes place when you move money from a traditional IRA to a Roth IRA, or from a Roth IRA to a traditional IRA. More specifically, recharacterization changes how specific contributions are designated depending on the type of IRA.

For example, maybe you believed your income would be too high to contribute to a Roth IRA in a specific year but found your income was actually low enough to contribute the full amount. If you already contributed to a traditional IRA, a recharacterization could help you move your funds into a Roth IRA, after all.

Of course, the opposite is also true. You might’ve thought your income qualified you to contribute to a Roth IRA but at the end of the year, you found out you were wrong after already making Roth contributions. In that case, a recharacterization to a traditional IRA could make sense.

These moves can be complicated, and there might be significant tax consequences along the way. It’s best to consult with a financial advisor or tax specialist before changing the designation of your IRA contributions and face potential tax consequences.

Early Withdrawal Penalties

You can withdraw your Roth IRA contributions at any time without penalty. Also, you can withdraw contributions and earnings 59 ½ and older, if you’ve had the Roth IRA account for at least five years. This is considered a qualified disbursement that won’t incur early withdrawal penalties.

But there are downsides if you need to withdraw your earnings ahead of retirement age. If you choose to withdraw your Roth IRA earnings before age 59 ½, you’ll face a 10% penalty. Some exceptions apply, though.

For example, you can withdraw earnings from your Roth IRA account without paying a penalty if you’ve had the account for at least five years, and you qualify for one of these exemptions:

- You used the money for a first-time home purchase,

- You’re totally and permanently disabled, or

- Your heirs received the money after your death.

Where to Get Help Opening an Account

If you feel like a Roth IRA is the best retirement vehicle for goals, you can open a Roth IRA account with almost any brokerage account. But they don’t all offer the same selection of investments to choose from. Some brokerage firms also offer more help creating your portfolio, and some charge higher (or lower) fees.

That’s why we suggest thinking over the type of investor you are before you open a Roth IRA. Do you want help creating your portfolio? Or do you want to select individual stocks, bonds, mutual funds, and ETFs and create your own?

Always check for investing fees as you compare firms, and the types of investments each account offers. We did some basic research for you to come up with a list of the best brokerage firms to open a Roth IRA.

- $0 per trade

- $0 mutual fund

- $0 set up

- 0.25% – 0.40% account balance annually

Bottom Line on Roth IRA Rules and Limits

Opening a Roth IRA is a great idea if you want to avoid taxes later in life, but you’ll want to start sooner rather than later if you hope to maximize this account’s potential. Remember that all of the money you contribute to a Roth IRA can grow tax-free over time.

Getting started now lets you leverage the power of compound interest to the hilt.Before opening a Roth IRA account, compare all of the top online brokerage firms to see which ones offer the investment options you prefer at fees you can live with. Also consider which firms offer the type of help and support you need, including the option to have your portfolio chosen for you based on your income, your investment timeline, and your appetite for risk.

Roth IRA Rules FAQs

Here are some of the key rules for a Roth IRA:

Eligibility: To contribute to a Roth IRA, you must have earned income and your income must be below certain limits.

Contribution limits: The maximum amount that you can contribute to a Roth IRA in a given year is set by the IRS and may change from year to year. For tax year 2023, the contribution limit is $6,500 if you are under the age of 50 and $7,500 if you are 50 or older.

Tax treatment: Contributions to a Roth IRA are made on an after-tax basis, meaning that you do not receive a tax deduction for your contributions. However, qualified withdrawals from a Roth IRA are tax-free.

Withdrawal rules: To make tax-free withdrawals from a Roth IRA, you must meet certain conditions. These include being at least 59 1/2 years old and having held the account for at least five years.

Required minimum distributions: Unlike traditional IRAs, Roth IRAs do not have required minimum distribution (RMD) rules, meaning that you are not required to take distributions from your Roth IRA at any specific age.

Rollovers: You can roll over money from a traditional IRA or another employer-sponsored retirement plan into a Roth IRA, but you may have to pay taxes on the amount rolled over.

While a Roth IRA can be a useful tool for saving for retirement, there are also some potential cons to consider:

Eligibility limits: Not everyone is eligible to contribute to a Roth IRA due to income limits. If your income is above a certain level, you may not be able to contribute to a Roth IRA or may be subject to reduced contribution limits.

Limited contribution room: The maximum contribution limit for a Roth IRA is lower than for some other types of retirement accounts, such as a 401(k). This may make it more challenging for high earners to save as much for retirement as they would like.

No upfront tax benefits: Contributions to a Roth IRA are made on an after-tax basis, which means that you do not receive a tax deduction for your contributions. This is different from a traditional IRA or a 401(k), which offer tax deductions for contributions.

Early withdrawal penalties: If you withdraw money from your Roth IRA before you reach age 59 1/2, you may be subject to a 10% early withdrawal penalty unless you meet certain exceptions.

Investment risk: As with any investment, there is the potential for the value of your Roth IRA to go down, either due to market fluctuations or poor investment choices. It is important to carefully consider your investment strategy and diversify your portfolio to manage risk.

The 5-year rule for Roth IRAs refers to the requirement that you must hold a Roth IRA for at least 5 tax years before you can make tax-free withdrawals of your earnings. This rule applies to both traditional Roth IRA contributions and Roth conversions (when you roll over money from a traditional IRA or employer-sponsored retirement plan into a Roth IRA).

If you do not meet the 5-year rule, you may still be able to make withdrawals of your Roth IRA contributions without penalty, but any earnings that you withdraw will be subject to income tax and the 10% early withdrawal penalty unless you meet an exception.

There are some exceptions to the 5-year rule that allow you to make tax-free withdrawals of your Roth IRA earnings before the 5-year holding period is up. These exceptions include:

First-time homebuyer: You can withdraw up to $10,000 in earnings tax-free and penalty-free to buy, build, or rebuild a first home.

Disability: If you become disabled, you can make tax-free and penalty-free withdrawals of your Roth IRA earnings.

Qualified education expenses: You can make tax-free and penalty-free withdrawals of your Roth IRA earnings to pay for qualified education expenses for yourself or a family member.

Cited Research Articles

- IRS.gov IRA Contribution Limits https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

- IRS.gov Roth IRA Income Limits https://www.irs.gov/retirement-plans/amount-of-roth-ira-contributions-that-you-can-make-for-2023

[ad_2]

Source link