[ad_1]

48% of Americans will need long-term care after reaching age 65. With the average cost of that coverage running between $3,600 and $7,700 per month, you should be making some provision to prepare for the possibility that you or your spouse will need some type of long-term care insurance coverage. For that reason, we’re presenting our list of the five best long-term care insurance of 2022.

Long-term care insurance is especially complicated because there are so many possible contingencies. The way to get the best policy is to discuss potential needs and options with several companies. You should then do a side-by-side comparison to determine which will provide the most benefits for the lowest premium.

The Most Important Factors for Long-term Care Insurance

When shopping for long-term care insurance, be sure to consider each of the following criteria in making your choice:

- Not all insurance companies offer long-term care insurance. It’s a highly specialized type of coverage with a relatively limited number of providers.

- Like all other types of insurance, the time to get long-term care insurance is before it’s actually needed.

- Premiums will be determined by a combination of your age, health condition, and the number and limit of benefits you want included in your policy.

- It may be more cost effective to choose either an annuity or a life insurance policy that has a long-term care provision. Though they are less benefit specific, premiums are generally lower.

- The maximum benefit you choose should approximate the cost of nursing home care in your area.

- It’s not possible to know how long long-term care insurance may be needed, so you’ll need to do your best to estimate how long that might be. Examples from your family lineage may provide guidance.

- Long-term care insurance policies typically come with an elimination period that requires the consumer to cover the full cost of care for the first few months it’s required. A shorter elimination period will require a higher premium. But you should have sufficient liquid assets to cover whatever the elimination period will be.

5 Best Long-term Care Insurance of 2022

GoldenCare Review

Based in Plymouth, Minnesota, and founded in 1976, GoldenCare is one of the nation’s largest privately held long-term care insurance brokerages. As a broker, they offer an opportunity to shop between multiple companies to find the best policy for you. The company offers their services in all 50 states.

When you work with GoldenCare, they’ll place your application with the company that will have the best long-term care policy for you. They work with some of the biggest companies in the industry, including Mutual of Omaha, Genworth, Humana, John Hancock, Aetna, Kemper and Humana. They also offer policies for critical care, critical illness, Medicare Advantage and Medicare supplements, prescription drug plans, life insurance, annuities, identity theft protection, and life/long-term care hybrids.

Pros and Cons

Pros

- Excellent source to locate the best long-term care policy without shopping among individual companies, one at a time.

- Policies available in all 50 states.

- Offers life/long-term care hybrid options that may be a better choice than a standalone long-term care policy.

- Excellent source to locate the best long-term care policy without shopping among individual companies, one at a time. Policies available in all 50 states. Offers life/long-term care hybrid options that may be a better choice than a standalone long-term care policy. A+ rating from the Better Business Bureau.

Cons

- Since GoldenCare is a broker, you won’t be dealing directly with the company other than to locate the most compatible provider.

- The website contains very little information about what types of plans are offered; you must contact the company to get that information.

LTCResourceCenters Review

LTCResourceCenters is a part of LTC Solutions, which is an independent managing general agency based in Cape Coral, Florida. The company has been in business for over 40 years and is licensed to provide policies in all 50 states. As an independent agency, the company can place your policy with any one of several insurance carriers they work with.

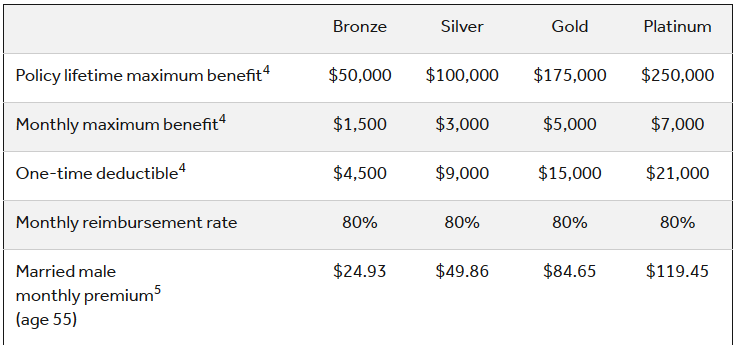

They provide both traditional long-term care insurance policies, as well as asset-based long-term care InsuranceAsset Based Long-term Care policies, giving you a choice of both benefits and premiums. An example of the two plans side-by-side is presented in the screenshot below, from their website:

Pros and Cons

Pros

- Opportunity to work with a broker that can offer you personalized long-term care policy options.

- Availability of several specialized long-term care insurance companies gives you a one-stop shopping advantage.

- Policies are available in all 50 states.

Cons

- Though the company operates nationally, it’s a single shot brokerage located in Florida.

- No list of partnering insurance companies is provided on the website.

- The company is not rated by the Better Business Bureau.

CLTC Insurance Services Review

California Long Term Care Insurance Services, Inc., or CLTC Insurance Services for short, is based in San Francisco and has been in business since 1997. In addition to long-term care insurance policies, they also offer life insurance with long-term care riders, annuities covering long-term care costs, life insurance covering long-term care costs, and critical illness insurance. Annuities and life insurance covering long-term care costs may be a more cost-effective way of preparing for long-term care for some consumers.

As a long-term care insurance aggregator, CLTC Insurance Services works much like GoldenCare and LTCResourceCenters in that they work with multiple providers. The policy you receive, as well as the costs and benefits offered, will vary by insurance company.

Pros and Cons

Pros

- As a long-term care insurance aggregator, CLTC Insurance Services can provide an opportunity to get the best plan for your needs and budget.

- They offer plenty of long-term care alternative plans, such as annuities and life insurance with long-term care provisions, which may work better for some consumers.

Cons

- CLTC Insurance Services appears to

- The website is vague as to plans and details.

- The company has an A+ rating from the Better Business Bureau.

Mutual of Omaha Review

Mutual of Omaha is one of the leading insurance companies in America and has been in business since 1909. As a large, diversified company, they provide virtually every type of insurance needed, as well as investment products. They’re one of the leading providers of long-term care insurance policies, and they offer their services in all 50 states.

Mutual of Omaha is a mutual insurance company, which means you as the consumer are an owner of the company – not just a customer. They also offer multiple discounts, particularly if you have other insurance policies with the company.

Pros and Cons

Pros

- As a direct provider, you’ll be dealing with Mutual of Omaha for your long-term care policy.

- The company offers a wide variety of benefit amounts, terms and elimination periods.

- Mutual of Omaha has an A+ rating from the Better Business Bureau.

- The company operates in all 50 states.

- As a full-service insurance company, Mutual of Omaha offers coverage of just about any type, as well as annuities and investments.

Cons

- Applying for coverage with just one company does not ensure that you’ll get the best policy for your needs and budget.

- If you apply with Mutual of Omaha and your application is declined, you’ll need to go on to another company.

New York Life Review

New York Life is a mutual insurance company, much like Mutual of Omaha, owned by its customers and not shareholders. Based in New York City, the company traces its origins all the way back to 1845. New York Life is one of the largest providers of long-term care insurance policies in America, and has partnered with the American Association of Retired Persons (AARP) as a preferred provider of these policies.

New York Life’s long-term care policies have one of the longest coverage periods in the industry, at up to seven years. They also pay one of the highest monthly benefits, at up to $12,000 per month. The company provides both traditional long-term care insurance, as well as a combination long-term care and life insurance option.

A sample of a NYL My Care plan, from the New York Life website, is presented below:

Pros and Cons

Pros

- Diversified insurance company that provides all types of policies, including long-term care insurance.

- You can choose either traditional long-term care insurance, or a life insurance/long-term care combination.

- The company has partnered with AARP to provide long-term care insurance policies.

- New York Life is rated A- by the Better Business Bureau.

- Provides coverage in all 50 states.

Cons

- The company gets only 2.5 out of five stars on Yelp, however, that’s based on just 13 reviews.

Getting Long-Term Care Insurance allows you to know that you’re protected as you age.

Long-term Care Insurance is beneficial for seniors and individuals with physical or cognitive disabilities. Purchasing a long-term care insurance policy ahead of time can help you save on the cost of premiums. Get a free quote today!

How We Found the Best Long-term Care Insurance of 2022

To come up with this list of the best long-term care insurance companies of 2022, we relied primarily on the following criteria (the first three providers in this guide don’t provide specifics because they work with multiple insurance companies, but you can choose a company offered by a broker or aggregator by the provisions they offer):

Specialization

We focused on the best feature each company provides. That will help readers and consumers to determine which company will be the best choice for their needs.

Maximum Benefit

You can expect the premium cost of a long-term care policy to be higher with a larger monthly benefit. But it helps to know what the maximum is, so you can match it with the expected cost of the care.

A policy with a maximum benefit of $2,000 per month will be insufficient to cover the cost of long-term care, if that cost averages, say $6,000 per month in your area.

Benefit Period

There’s no way to know how long you may need long-term care. But having a longer-term, one covering at least several years, will offer greater protection.

Elimination Period

Though a shorter elimination period will require a higher premium, it’s important to have that option. If you have sufficient liquid assets to cover, say six months of long-term care costs, you might go with a six-month elimination period. We favored companies that offer multiple elimination periods.

BBB Rating

While it’s common to use independent financial rating services (like A.M. Best) when it comes to insurance companies, we felt it more important to include ratings from the Better Business Bureau.

While these ratings don’t indicate the company’s financial strength, they do indicate consumer experience. A higher rating means consumers are generally satisfied with the services the company provides. This will include the willingness of the company to pay benefits, among other factors.

What You Need to Know About Long-term Care Insurance

Because of the contingent nature of long-term care, long-term care insurance policies tend to be more complicated than other types of insurance.

Factors to be aware of include:

- Cost. Long-term care insurance can cost several thousand dollars per year. Premiums rise with age, as well as with the benefit level selected.

- It’s possible you may never need the policy. As noted at the beginning of this guide, about 48% of Americans over 65 will need paid long-term care assistance. But that means 52% won’t. You may be paying for a policy you’ll never use.

- Long-term care insurance isn’t the only option. Many insurance companies now offer annuities and life insurance policies with long-term care provisions. They’re generally less expensive than the premium you’ll pay for a traditional long-term care policy.

- You need to qualify for long-term care benefits. Before you’ll be eligible, you generally must be unable to perform at least two of the six activities of daily living (ADLs).

- Long-term care policies offer a variety of riders. For example, an inflation rider can be added to accommodate higher costs in the future. A return of premium rider provides for some or all the premiums paid on a long-term care policy to be paid to beneficiaries upon the death of an insured who never needed the coverage. These riders will increase the premium.

- There are several different types of long-term care. Though the classic example is a nursing home, other options include assisted living, hospice care, and in-home care. Be sure the policy you select will extend coverage to each of these options.

What is the best age to buy long-term care insurance?

Though financial advisors typically advise taking a policy between the ages of 55 and 65, it can be desirable to apply sooner. Like any other type of insurance, it’s always best to apply when you’re younger and healthy. Both your age and your health status at the time of application will affect both approval and premiums.

What is the average cost of long-term care insurance?

What health conditions disqualify you for long-term care insurance?

If you’re in generally good health at the time of application, your application should be approved. But if you are currently experiencing Alzheimer’s, Parkinson’s disease, or certain forms of cancer, your application may be declined. Other possibilities include regular use of a walker, or currently needing help with any of the six activities of daily living (ADLs).

What is the best long-term care policy company?

There is no company that provides the best policy for all consumers, or even most. To find the best policy, you’ll need to determine what your long-term care needs and expectations are, what benefits you want to receive, as well as the cost for the policy. Long-term care policies are highly customized, so it’s impossible to generalize which company your policy will be the best one in your situation.

Does Medicare cover the cost of long-term care costs?

[ad_2]

Source link